The Federal Open Market Committee (FOMC) meeting that concluded on March 16 was much anticipated by market participants. Speculation going in was that the FOMC would begin raising the target overnight rate and the committee didn’t disappoint, raising the Fed Funds target range from 0-.25% to .25%-.50%. This was the first Fed rate hike since the end of 2018. The complete press release from the Federal Reserve can be found here.

For the most part, the information presented during the meeting was predigested with the commentary serving as an interesting side note to market participants as investors tried to get a better idea of the future path of interest rates from comments by Federal Reserve Chairman Jerome Powell. In this article, we will discuss some of the takeaways from the meeting, what transpired in the week following, and the reaction of the bond market.

Quarterly Economic Update Webinar

To hear comments on this month’s FOMC meeting from Corporate One’s Chief Investment Officer Bob Post, watch the on-demand version of the webinar, which aired live on March 17.

Reviewing the dot plot forecast

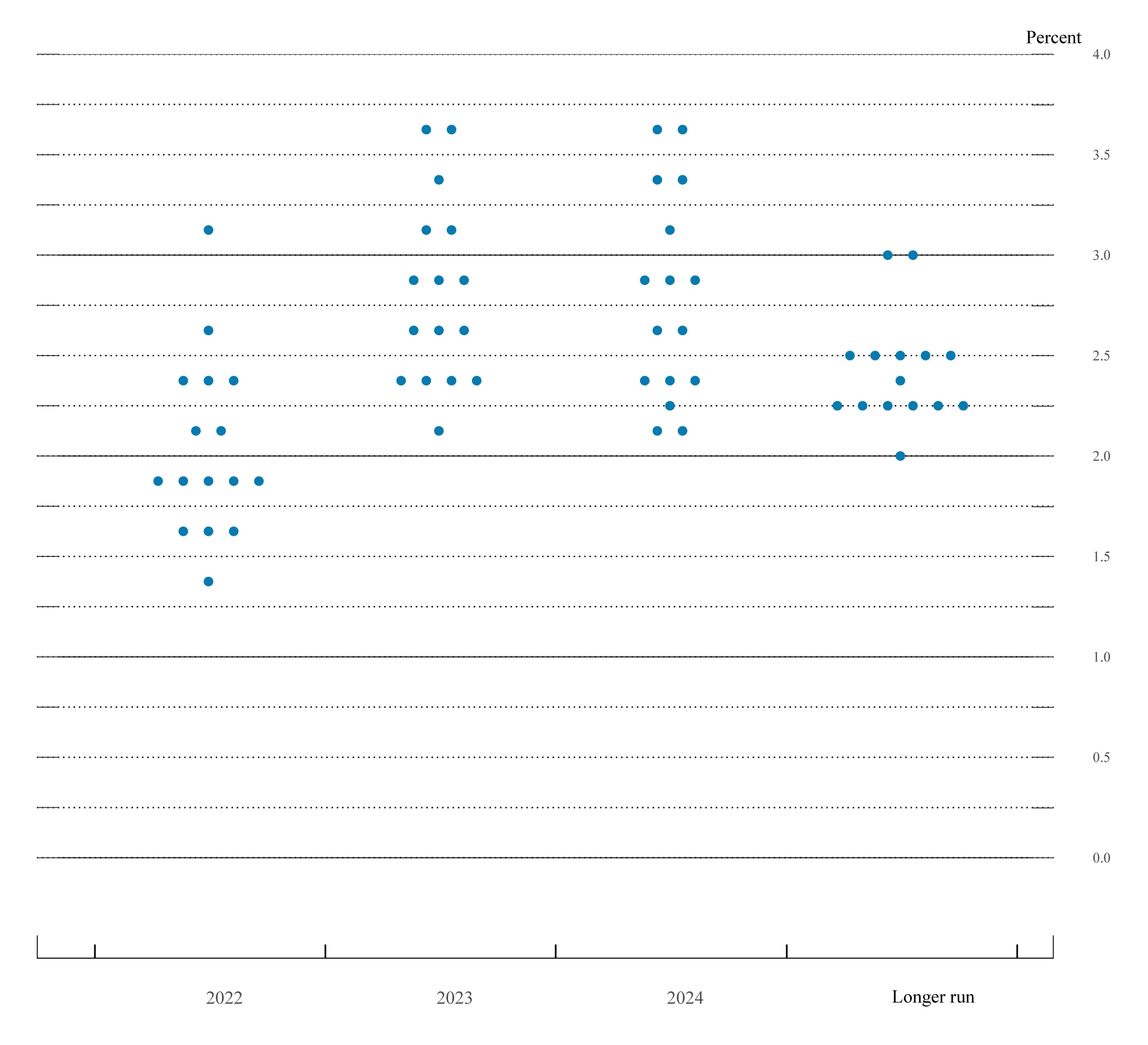

We would be remiss to write a follow up to a Fed meeting without including the dot plot. As a reminder, the dot plot is simply a chart that summarizes the FOMC’s outlook on interest rates. Up to 19 Fed officials can contribute their perspectives, and they do so anonymously. The dot plot is released every three months, and March’s dot plot is below.

This dot plot is calling for a total of seven rate hikes in 2022. This is consistent with statements following the meeting as well, but the consensus from the dot plot of just over 1.75% would be 7- 25 basis point hikes. We will see if this is updated next time as more talk is devoted to more aggressive hikes. You can view a summary of economic projections from the March meeting here.

Four highlights from the FOMC press conference

- Regarding economic strength, Powell said twice at the beginning of the conference that the economy is very strong. He also added that the demand for labor was strong and the labor market is extremely tight.

- In response to questions about recession, Powel stated, “In my view the probability of a recession within the next year is not particularly elevated.” Powell noted that households and businesses are in good financial shape and should be able to withstand the proposed future rate increases, which reiterated the strength of the economy.

- Powell noted that inflation was strong, too, and “imposes significant hardship, especially on those least able to meet higher cost essentials.” The FOMC also lifted its expectation for inflation for 2022. The core personal consumption expenditures price index (PCE) projection went from 2.7% in December 21 to 4.1%, and the FED sees relief kicking in in 2023 but projecting down to 2.6% above the 2% target.

- In speaking about the balance sheet, Powell also stated that conversations were had to tee up reducing its size. This would include selling longer-dated securities accompanied by not reinvesting principal from maturities.

Post-meeting chatter

After the FOMC meeting, the bond market sold off, especially on the short end. This was followed by a rally as information was further digested. At the beginning of the week of March 21, Powell, while speaking at the national Business for Economics, took an even more hawkish tone. He conceded that Fed officials and many economists underestimated how long inflationary pressures would last. He also stated that the labor market is very strong, and inflation is much too high. The chairman vowed that the FOMC will take the necessary steps to move the economy back to price stability, stating that the FOMC might need to move more aggressively by raising the Federal Funds rate by more than 25 basis points. Other Fed officials echoed this statement in the days following with St. Louis Fed President James Bullard stating on Bloomberg TV that “faster is better” when it comes to rate hikes and that 50 basis point moves should definitely be in the mix.

Reactions from the market

As mentioned previously, the bond market sold off following the meeting but eventually settled down as more information was digested. The week following Powell’s comments was a bit more volatile. The yield curve itself has probably acted as it should, following a rate hike with short-end rates moving up at a faster pace than longer-term rates. The curve steepens between 1 and 3yrs and then begins to flatten with the 3yr and 5yr treasuries trading around parity. Then the curve begins to invert with the 10yr U.S. Treasury trading at a lower yield than shorter maturities.

Opportunities for credit unions

Credit unions should continue to take a balance-sheet-specific approach to investing, and portfolio laddering is best recommended. Presently, the yield curve offers the best opportunities up to three years as the flat yield curve doesn’t “pay investors” to go out longer. The volatility in the market has created some opportunities in callable agency bonds as higher volatility increases the cost of the optionality of the bond. To take on the additional call risk, investors are demanding a higher yield and spread exists between callable issues and noncallable issues. We continue to see investor interest in U.S. Treasuries for safety, availability, and liquidity. We also see investors continue to purchase amortizing bonds, like mortgage-backed securities, that allow for reinvestment of principal over time as it is returned. Mortgage bonds will continue to see slower paydowns as refinancing of homes lessens, which offers a bit more predictability in regard to cash flows.

For specific offerings, please reach out to your senior investment services representative. You can also sign up to receive daily notifications of investment rates, securities rates, special structured offerings, and more here.

To get inflation under control, an admittedly behind FOMC will need to be aggressive in raising rates throughout 2022. Seven hikes total is likely a safe bet, and the question is “will this be 25 basis point hikes, .50%, or a combination of both? Your credit union can expect to earn more on investments and new loans and, hopefully, grow net interest margin.

Disclaimers

All securities are offered through Multi-Bank Securities, Inc. (MBS). The home office of MBS is located at 1000 Town Center, Suite 2300, Southfield, Michigan 48075. MBS is registered with the Securities and Exchange Commission (SEC) as a broker-dealer under the Securities Exchange Act of 1934. Member of FINRA and SIPC. MBS’s FINRA Broker-Dealer CRD number is 22098.

Jeff Duesler

Senior Investment Services Representative