Corporate One headquarters in Columbus, Ohio

Currently serving more than 730 credit unions nationwide, Corporate One is one of the nation’s largest and most trusted corporate credit unions. For 75 years, we’ve been creating opportunities for credit unions to succeed through our premier investment, funding, and payment solutions.

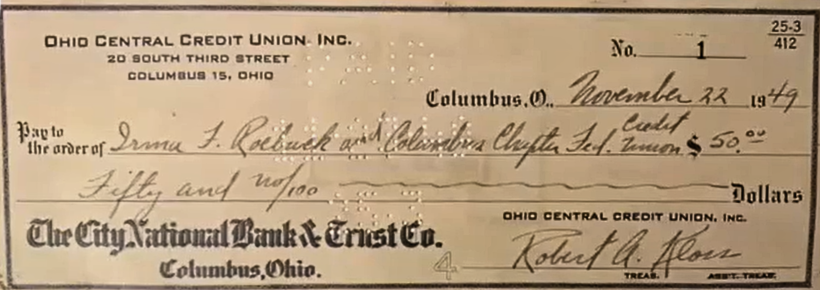

Our Origins as a Credit Union for Credit Unions

Founded in 1949 as Ohio Central Credit Union, our organization was chartered as a “credit union for credit unions,” based on the traditional principles of service to members that guide all credit unions. Ohio Central served two distinctly separate groups: Ohio credit unions, receiving the services of a corporate central credit union, and natural person members. At the time, such a credit union was known as a “dual corporate central credit union.”