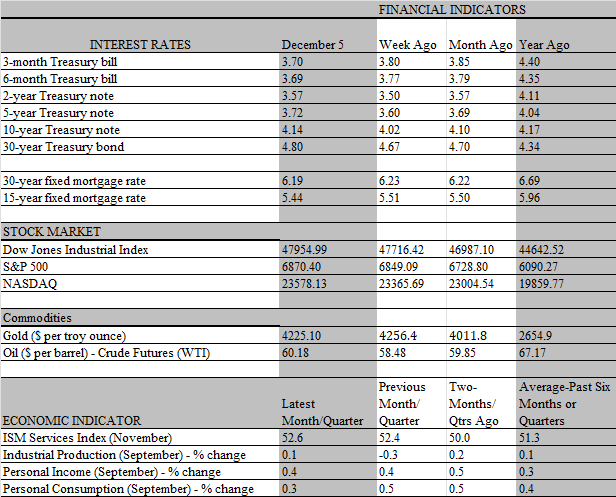

The hoopla commanding headlines this week centered on the Federal Reserve, which held its second FOMC meeting under the new Chair, Kevin Warsh. As mostly expected, policy makers decided not to take away the punch bowl, opting to keep rates unchanged at the same 3.50-3.75 percent in effect since January. There was more than a non-trivial chance that the Fed would hike at the meeting, which in fact three of the twelve members of the FOMC voted for to check inflation. We agree with the majority vote. While inflation is still running well above the 2 percent target, that’s not because the economy is overheated, usually a requisite condition to justify a rate increase. Indeed, the financial markets interpreted the comments made by Warsh in the post-meeting press conference to be somewhat dovish and priced in lower odds of an increase at the September meeting than before but retained high odds that one would be forthcoming before the end of the year.

That said, Warsh seems to have mastered the art of obfuscation, echoing the celebrated linguistic prowess of former Chair Alan Greenspan who famously said at a congressional hearing: “If I seem unduly clear to you, you must have misunderstood what I said.” There was little chance of that happening at this presser, as reporters as well as market participants are totally uncertain what the next Fed move would be – or what conditions would be necessary to move the needle. The absence of a reaction function to work with opens the door to heightened speculation among traders following each data point, something that is likely to stoke more volatility than otherwise. Of course, that is Warsh’s intention as he is firmly against giving forward guidance to the markets. Instead, he would prefer that market participants draw independent conclusions from the data, which, in turn, would recycle valuable information back to the Fed.

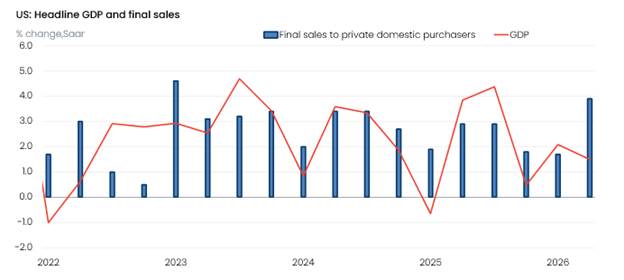

The raft of economic data this week neither supports nor invalidates the “wait-and-see” posture delivered at the Fed meeting. On the surface, conditions appear to have cooled a bit in the second quarter, as headline GDP slowed to a 1.5 percent growth rate from 2.1 percent in the first quarter. But under the hood just the opposite is the case. All of the slowdown reflected stronger imports, which replaces domestically produced output, and an inventory drawdown. But the mirror image of those drags depicts strength, as final sales to private domestic purchasers jumped by 3.9 percent from 1.7 percent. Much of those purchases were from foreign producers of computer chips, semiconductors and other inputs that feed into the AI spending boom. That, paired with purchases that came from inventories instead of newly produced goods, accounted for all of the drag from the first to the second quarters.

Importantly, consumers regained the mantle of growth in the second quarter, contributing almost twice as much oomph to GDP than investment spending, the pacesetter during the previous quarter. To be sure, business spending retained its vigor as the AI buildout continued apace and added about as much to GDP as it did in the first quarter. But it also consumed a lot of imports, which had an offsetting drag on headline GDP. On the other hand, consumer spending rebounded strongly from the first quarter malaise, which was hampered in good part by harsh weather that impeded visits to restaurants and other service-providing establishments. But those outlays were deferred, not destroyed, and they came roaring back in the second quarter. Personal consumption grew by a torrid 3.2 percent annual rate during the period following a meager 0.5 percent advance in the first quarter.

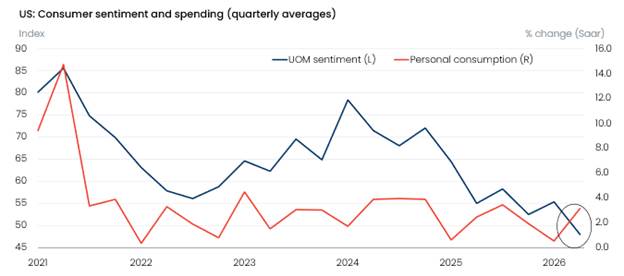

The rebound was juiced not only by the return of normal weather but also by the considerable financial support from above average tax refunds. A temporary decline in gas prices in June also freed up funds for lower income households to spend on other goods and services. We note, however, that the disconnect between how consumers feel and behave widened in the second quarter. Even as spending rebounded, consumers turned more despondent over elevated prices, high borrowing costs and lowered expectations of job and income prospects.

No doubt, the widening disconnect between feelings and behavior was driven by noise as well as substance, as the escalation of Mideast hostilities inflamed uncertainty and worries over the sustained high level of gas prices and utility bills. It’s important to remember, however, that every household respondent to surveys carries an equal weight, whereas only 10 percent of consumers account for about 50 percent of spending. The purchasing power of that affluent 10 percent, meanwhile, is heavily linked to the performance of their stock portfolios, which delivered another impressive 15 percent gain in the second quarter, generating nearly $9 trillion of additional wealth.

While the wealth effect pumped up consumer spending in the second quarter, there is no guarantee it will continue to be as potent a driver going forward. The stock market has had a rocky start so far in the third quarter, reflecting growing concerns over whether the returns will justify the overzealous spending by tech companies, which are delving deeply into free cash flow and borrowing heavily to finance expansion plans. Still, barring a confidence-shattering and outsize wealth-destroying setback in stock prices, spending by upper-income shareholders should hold up. Affluent households have built up a formidable cushion of asset values to tide them over a bout of adversity.

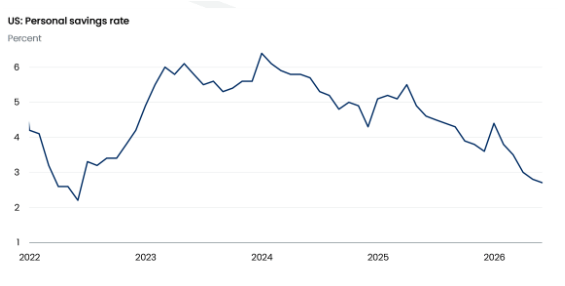

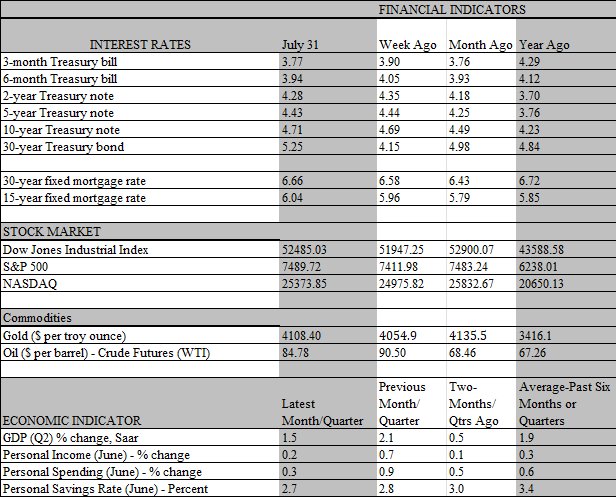

Not so for those lower down the income scale. This cohort has drawn heavily on savings to support spending, what’s more, those whose wealth is mostly tied up in home equity have seen little appreciation this year even as they are locked in from cashing out by high mortgage rates. National home prices, according to the Case-Shiller National Home Price Index, is up 1.1 percent over the past year. But inflation is up 3.7 percent according to the latest personal consumption deflator, so homeowners are sitting on a depreciating asset in real terms. Meanwhile, the personal savings rate fell to a six-year low of 2.7 percent in June, suggesting little in the form of liquid assets to cushion the blow from a possible economic setback leading to job losses. We expect households not on the top 10 percent rung of the income ladder to build up precautionary savings, an effort that will be a drag on consumer spending over the second half of the year. That, in turn, should further defuse notions the economy is overheating and keep the Fed’s finger off the rate-hiking trigger this year.